Navigating Philippine government regulations to get employee wages, contributions, and taxes right can be complex. One wrong move and you could be facing hefty fines and disgruntled employees.

To help you stay perfectly compliant with dynamic Philippine tax laws and compensation packages and to ensure a smooth payroll process, we’ve prepared this helpful guide.

Working Conditions and Rest Periods

Let’s start by understanding the key regulations set by the Department of Labor and Employment (DOLE) regarding Working Conditions and Rest Periods, as outlined in the latest Labor Code of the Philippines (2022 Edition).

Chapter I – Hours of Work

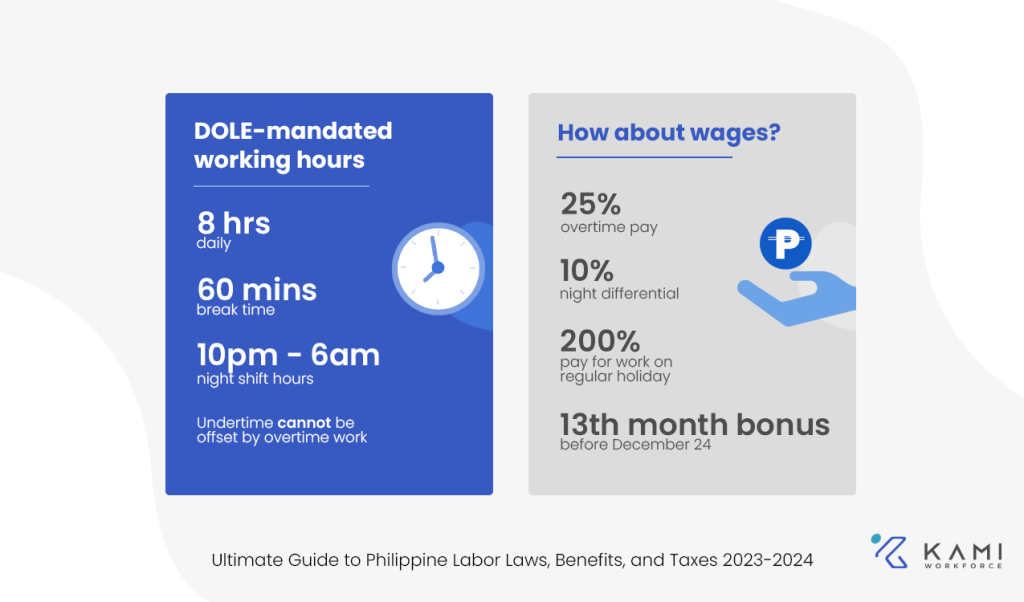

83. Normal Hours of Work – should not exceed eight (8) hours per day.

85. Meal Periods – not less than sixty (60) minutes time off for their regular meals.

86. Night Shift Differential – not less than 10% more than their regular wage for each hour performed between 10 pm – 6 am.

87. Overtime Work – 25% more than the regular wage for work performed beyond 8 hours per day. 30% more than the holiday or rest day rate for overtime on those days.

88. Undertime Not Offset by Overtime – undertime on any day cannot be offset by overtime on any other day.

90. Computation of Additional Compensation – the “regular wage” for purposes of calculating OT and other additional remuneration shall include the cash wage only.

💡Note: This typically means their base salary sits at a minimum, with other benefits such as allowances only to be included at the employer’s discretion.

Chapter II – Weekly Rest Periods

91. Right to Weekly Rest Day – not less than twenty-four (24) consecutive hours after six (6) consecutive normal workdays.

92. When Employer May Require Work on a Rest Day – when there is an emergency, urgent work, abnormal pressure to prevent loss, or where work requires continuous operation.

93. Compensation for Rest Day, Sunday, or Holiday Work – 30% more than the regular wage for work on a rest day or special holiday. 50% more if it is a rest day and a special holiday.

Chapter III – Holidays, Service Incentive Leaves, and Service Charges

94. Right to Holiday Pay – Every worker shall be paid their regular daily wage during regular holidays, except in retail and service establishments regularly employing less than ten (10) workers; 200% of the regular wage shall be paid for any work on any holiday.

Holidays include – New Year’s Day, Maundy Thursday, Good Friday, the ninth of April, the first of May, the twelfth of June, the Fourth of July, the thirtieth of November, the twenty-fifth and thirtieth of December, and the day designated by law for holding a general election.

94. Right to Service Incentive Leave – Every employee who has rendered at least one year of service shall be entitled to a yearly service incentive leave of five (5) days with pay.

💡Note: Service Incentive Leave is equivalent to “Annual Leave” or “Vacation Leave”. Provision of Sick Leave is not mandatory, however, employers often provide this incentive.

131. Maternity Leave – pregnant (female) employees who have rendered an aggregate service of at least six (6) months for the last twelve (12) months, are allowed maternity leave of at least two (2) weeks before the expected date of delivery and another four (4) weeks after normal delivery or abortion with full pay based on her regular or average weekly wages.

💡The country has also introduced the Expanded Maternity Leave, which allows up to 105 days (15 weeks) maternity leave.

The following additional leaves have also been granted under other specific laws defined outside of the DOLE Labor Code.

Parental Leave (R.A. No. 8972, Solo Parents’ Welfare Act) – seven (7) days paid leave granted to a solo parent to enable him/her to perform parental duties and responsibilities where physical presence is required

Battered Woman Leave (R.A. No. 9262, Anti-Violence Against Women and their Children Act of 2004) – paid leave of absence up to ten (10) days, extendible when the necessity arises as specified in the protection order.

Gynecological Disorders (R.A. No. 9710, Magna Carta of Women) – two (2) months with full pay after a surgery caused by gynecological disorders

Paternity Leave (R.A. No. 8187, Paternity Leave Act of 1996) – A married male employee shall be granted seven (7) days with full pay for the first four (4) deliveries of the legitimate spouse with whom he is cohabiting.

Wages

99. Regional Minimum Wages. Are prescribed by the Regional Tripartite Wages and Productivity Boards.

💡Note: The National Capital Region, where the city of Manila is located, requires a minimum wage of ₱533 – ₱610 for the non-agricultural sector and ₱533 for the agricultural sector.

For the full list of daily minimum rates as of 2023, visit the Department of Labor and Employment.

103. Time of Payment. Wages shall be paid at least once every two (2) weeks or twice a month at intervals not exceeding sixteen (16) days.

113. Wage Deduction. Wages may only be deducted for a) insurance premiums, b) union duties, and c) authorized by law.

💡Note: Reduction of wages due to any tardiness or absence from work is not considered a wage deduction.

13th Month Pay

Under Presidential Decree 851, 13th-month pay is a mandatory benefit for employees in the Philippines, provided the employee has worked with your company for at least one (1) month during the calendar year.

It is calculated by totaling the Basic Salary earned in the calendar year and dividing it by 12 months.

13th-month pay = Total Basic Salary / 12

💡Note: Basic Salary excludes any OT, rest day pay, holiday pay, or leave encashments. Any deductions to regular basic salary for unpaid leaves or absence from work should also be included.

13th-month pay is only taxable if the amount exceeds the non-taxable threshold of ₱90,000.

Mandatory Employee Contributions in the Philippines

Social Security System (SSS)

SSS is the national social insurance program that administers the pension fund as well as a variety of social security benefits such as sickness, retirement, maternity, disability, and death benefits.

The employer is required to remit to SSS on behalf of the company and employees.

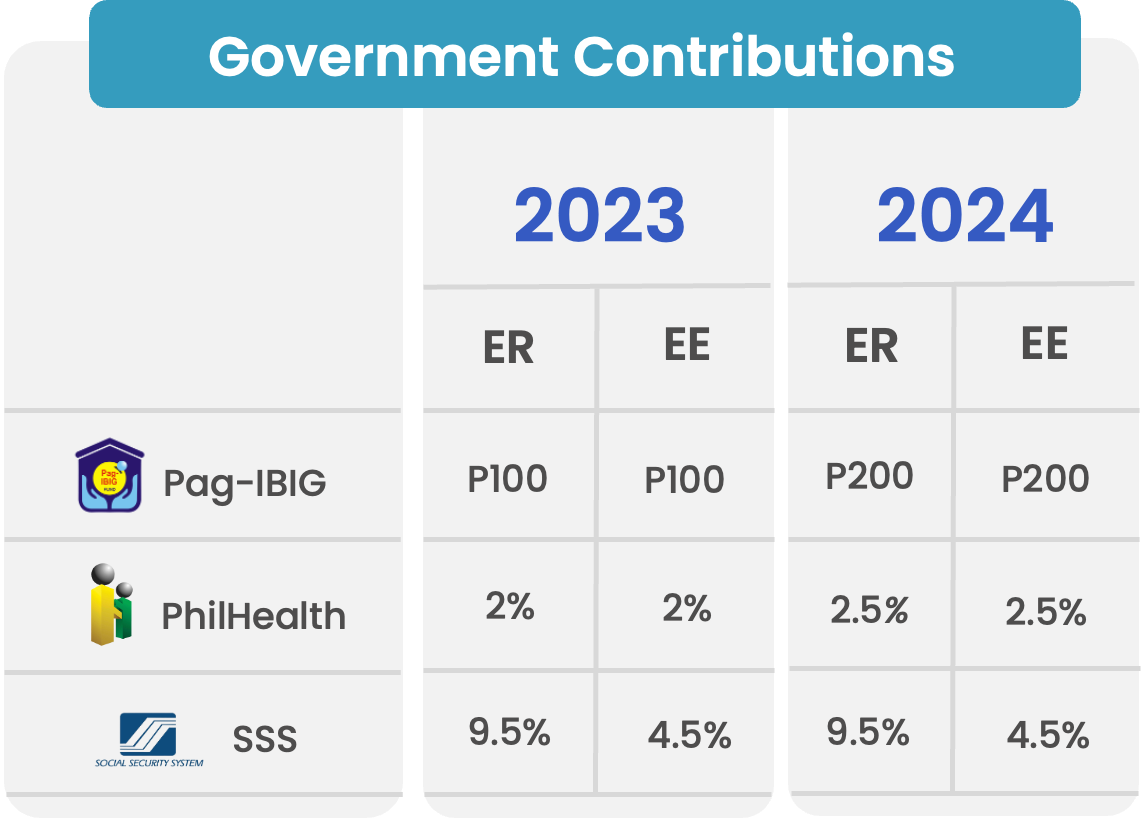

As of 2023, SSS has set its monthly contribution rate to 14% of Monthly Salary Credit (MSC).

💡Note: Monthly Salary Credit is based on the total monthly wage, which includes wages in addition to basic wage, such as OT, rest day pay, and holiday pay.

💡It also includes deductions for unpaid leaves and absences.

Employer contributions currently stand at 9.5% while employees contribute 4% according to the SSS table.

Other computations you should understand about SSS are Employees’ Compensation (EC) and the Workers’ Investment and Savings Program (WISP).

EC is a program set by the SSS to assist workers who suffer work-related sickness resulting in disability or death. It is added to the employer’s share at ₱10 for MSC below ₱20,000 and ₱30 for MSC above that level.

WISP is a compulsory provident fund that can be claimed as a lump sum or annuity. All employer and employee SSS contributions for MSC above ₱20,000 are allocated to WISP.

Philippine Health Insurance Corporation

PhilHealth is a national health insurance program. Members (and registered dependents) get access to healthcare coverage and medical services, including hospitalization, check-ups, and treatments.

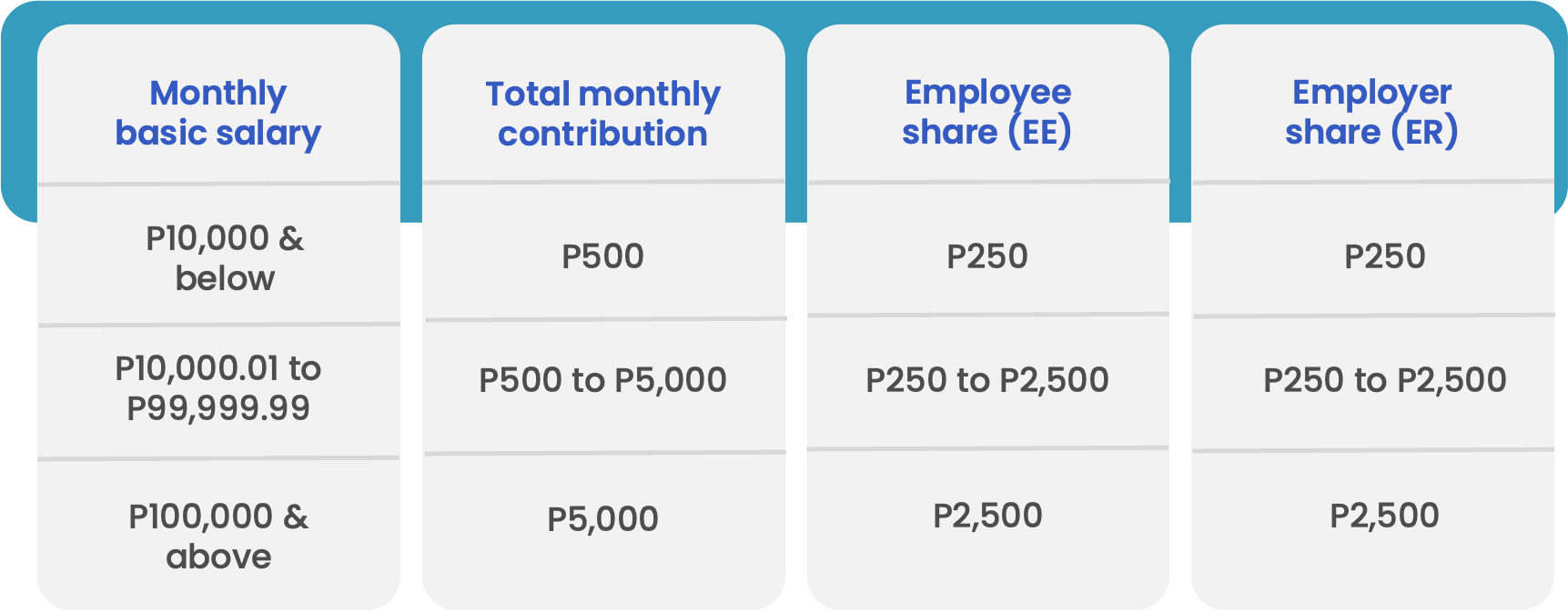

In 2023, the total contribution rate is 4% of the base salary, evenly split at 2% each between the employer and employee, and subject to an income cap of ₱80,000.

However, the rates have since increased in 2024:

- For employees earning an income of ₱10,000 a month, their PhilHealth contribution will be ₱500.

- For employees earning ₱10,000.01 to ₱99,999.99 a month, deductions ranging from P500 to P5,000 shall apply.

- Those earning ₱100,000 contribute ₱5,000 to PhilHealth monthly.

For a year-on-year analysis of PhilHealth contributions, view the official guide from the state insurer.

Home Development Mutual Fund (Pag-IBIG)

The Pag-IBIG fund, officially known as the Home Development Mutual Fund (HDMF), is another government agency in the Philippines that provides financial assistance for housing and multi-purpose loans.

In 2023, employees with a fund salary of ₱1,500 contribute 1%, and 2% if they’re earning more than ₱1,500 per month. Employer shares were fixed at 2%, regardless of the employee’s salary.

It’s worth noting that Pag-IBIG contributions and regulations will undergo updates by February 2024, changes were delayed from 2021 due to the pandemic:

- Maximum Fund Salary (MFS) is to increase from ₱5,000 to ₱10,000.

- Pag-IBIG shall implement a contribution hike from 1% to 2% (₱100 to ₱200).

Employers shall continue to remit 2% of the MFS on behalf of the member as a counterpart contribution. This should not be deducted from the employee’s wages or remuneration.

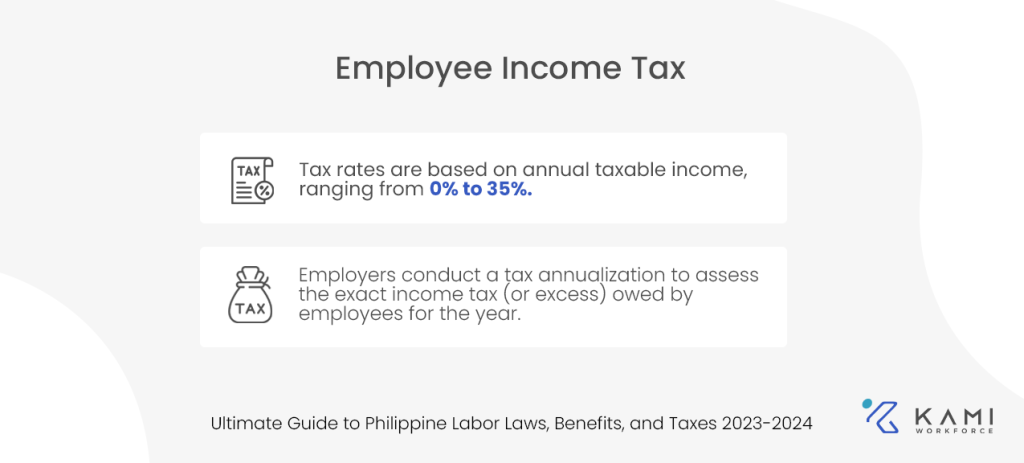

Employee Compensation Income Tax

Employers do not contribute to their employees’ income tax. They are, however, required by the Bureau of Internal Revenue (BIR) to act as a withholding agent and are obligated to deduct and remit income taxes from their employees.

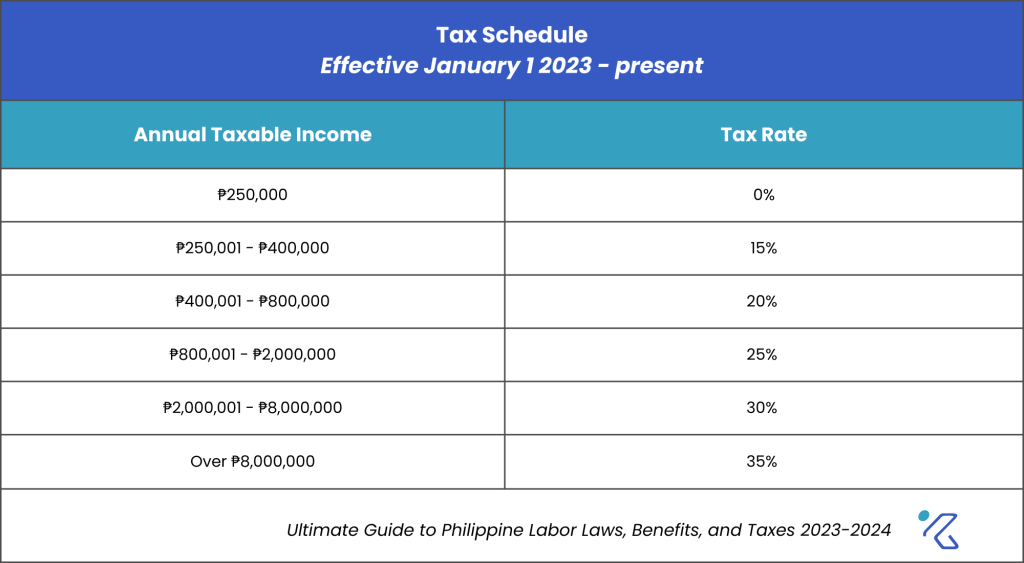

Under the Tax Reform for Acceleration and Inclusion (TRAIN) law, Filipino employees earning an annual income of more than ₱250,000 are required to pay taxes.

Tax schedule effective January 1, 2023, to present, courtesy of the Department of Finance.

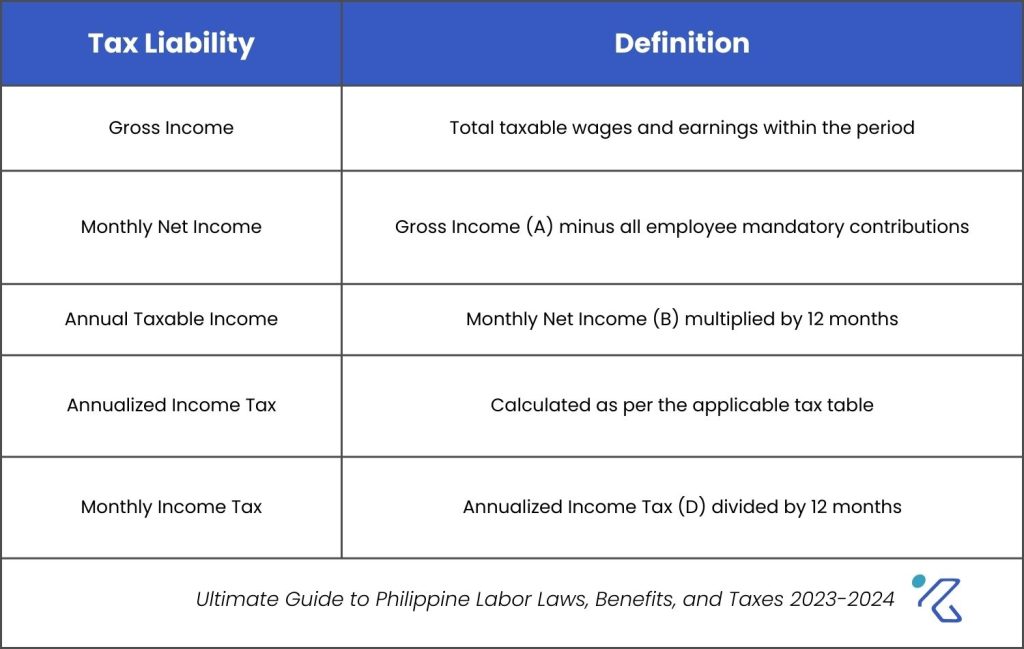

Withholding Monthly Income Tax

Income tax is required to be withheld and remitted by the employer every month based on an estimate of monthly tax liability outlined below.

Thus, the monthly tax withheld is based on an annualized estimate.

💡Note: Bonus payments should be added to Annual Taxable Income, subject to the ₱90,000 non-taxable threshold.

Year-End Income Tax Adjustment

Employers are required to complete a tax annualization to determine the exact income tax due from employees for the year, and if any excess or shortfall exists from the estimated amounts withheld on a monthly basis.

Refer to the official BIR website for the latest calculations for year-end tax adjustments.

Employee Termination & Separation

Final pay, as defined by the Labor Advisory No. 06-20 issued by the Department of Labor and Employment, is the “sum or totality of all wages or monetary benefits due to the employee regardless of the cause of the terminal of employment.”

It includes but is not limited to the following:

- The employee’s unpaid salary;

- Cash conversion of unused Service Incentive Leave (SIL) pursuant to Article 95 of the Labor Code;

- Pro-rated 13th-month pay, in accordance with Presidential Decree No. 851 (PD 851);

- Where applicable, terminated employees are entitled to separation pay pursuant to Articles 298-299, as renumbered by company policy or individual agreement;

- Retirement pay in accordance with Article 302 of the Labor Code, if applicable;

- Income tax for the excess of taxes withheld, if applicable;

- Other compensation is set in an individual or collective agreement, as well as cash bonds or deposits due for return to the employee, if any as stated in Section 2, Article I, DOLE Labor Advisory No. 06, Series of 2010, henceforth “DOLE LA 06-10”.

Best Practices to Get Your Philippines Payroll Right!

Have good policies

Take the time to learn about what the government requires and what other compensation you want to provide your people. Having clear, well-documented policies that are properly communicated and consistently applied is critical.

Invest in technology

Automate payroll calculations with quality payroll software from a reputable provider to ensure your data is well-maintained and secure, processes are streamlined, and human error or intervention is minimized.

Ensure accurate timekeeping

Keeping track of time worked, leaves, absences, OT, holiday pay, etc… is often the most challenging part when processing payroll. Ensure you have a system that can accurately record and feed timekeeping data directly into your wage calculations without manual intervention.

Automate calculations

Get away from Excel worksheets, as they are prone to human error and unwanted intervention. A good payroll system should automatically make all the calculations for you, leaving you to only handle any special situations.

Multi-tiered Validation and approvals

Multi-tiered validation reduces the risk of fraud and error. It also promotes accountability, with each individual involved in the process ensuring that the data complies with regulations.

Keep an audit trail of payroll records

Employers are required by Philippine labor laws to preserve employee records, including payroll records, for at least three years.

Take note of termination and severance policies

In cases where an employer terminates a work agreement, owing to reasons such as retrenchment or business closures, they are obliged to provide a separation pay constituting at least one month’s pay or at least one-half of one month’s pay for every year of service, whichever is higher.

Employees who voluntarily terminate their employment are not entitled to severance pay.

Keep Up With Regulatory Changes

Ensuring that your payroll process adheres to the Philippine labor legislation helps you avoid noncompliance penalties that could lead to business closure, fines, or imprisonment.

But with the sheer number of labor laws and regulations, how do you keep your company in compliance?

KAMI might just have the solution for you. As an integrated HR platform, you get everything you need to track attendance and disburse payroll in accordance with the latest regulations.

Talk to an expert today to learn more.