As 2024 lands on our feet, employers in Indonesia need to recalibrate their focus toward year-end payroll duties. There are regulations to stay on top of and tax duties to fulfill.

Of that note are the recent changes in Indonesia’s withholding tax laws, which require close attention from businesses and their finance teams.

To help you stay on top of the latest regulations, we’ll delve into the latest changes and highlight other year-end tax requirements in this article.

Note that our article only covers year-end tax requirements for withholding agents.

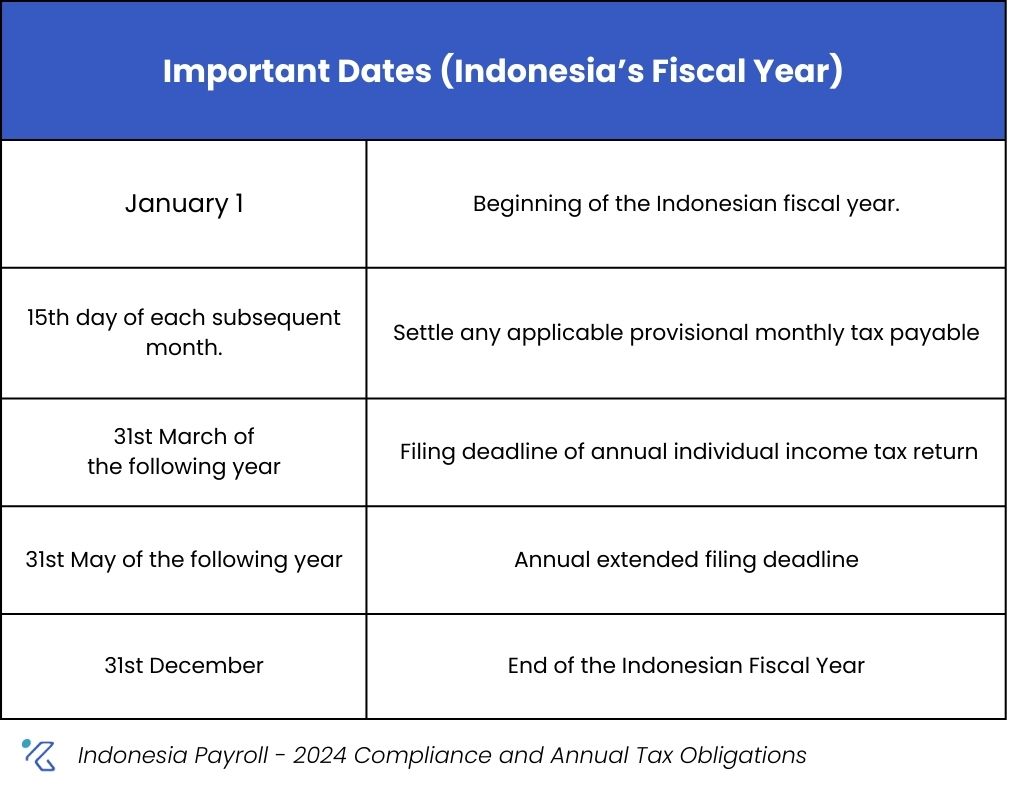

Fiscal Year – Indonesia

Indonesia’s fiscal year coincides with the calendar year.

Throughout this period, tax liabilities are settled with the State Treasury via a designated tax-payment bank (‘bank persepsi’). Transactions are then accounted for by the Directorate General of Taxes (DGT).

Annual Employer Tax Obligations 2023-2024

1. Estimate Withholding Tax (Article 21 – Income Tax)

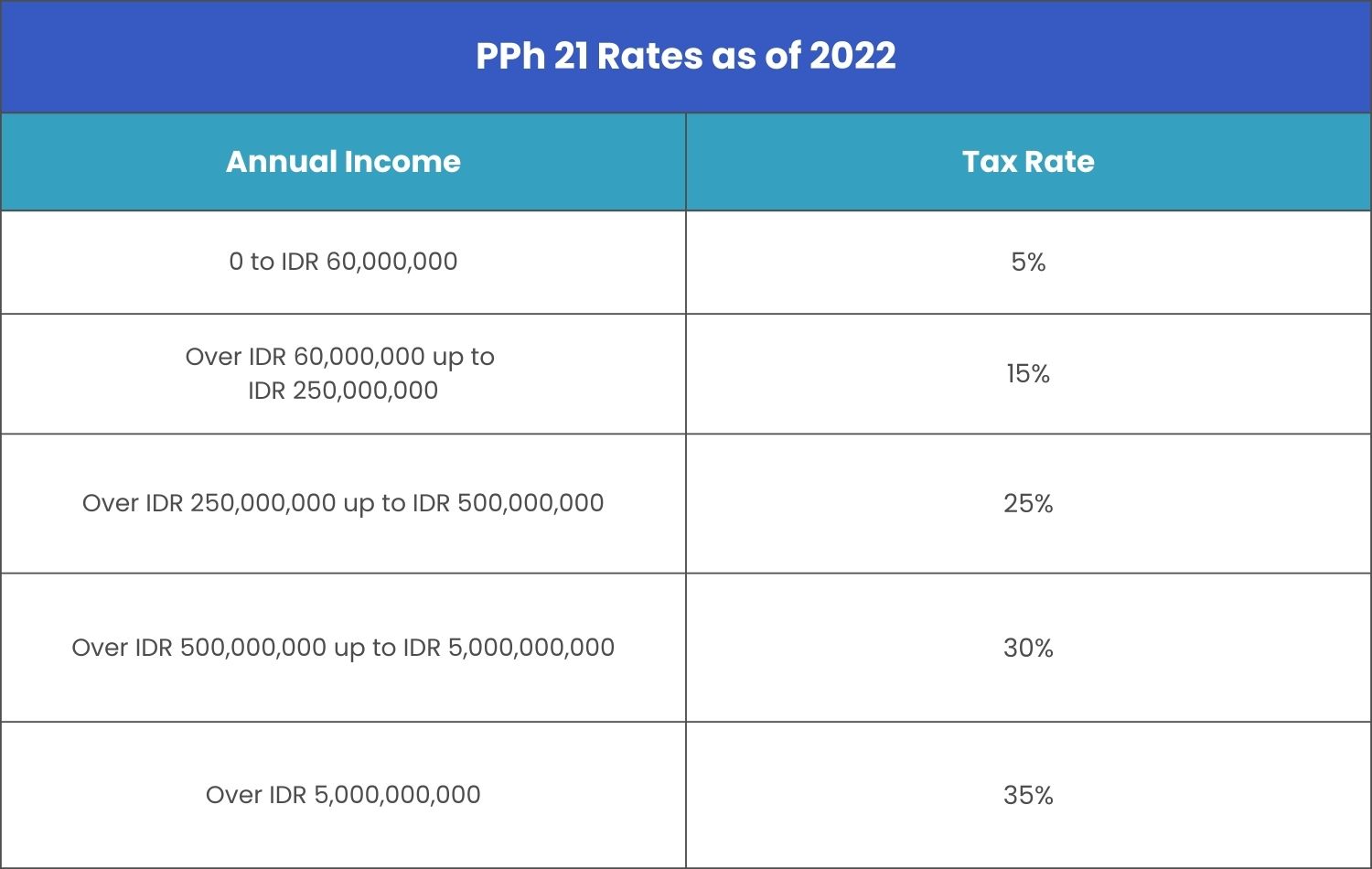

Income Tax Article 21 (PPh 21) is tax withheld from earnings tied to work and services rendered in Indonesia. Previously, individual income tax was subjected to 5% to 35% progressive income tax rates.

However, on December 27, 2023, the Indonesian government announced Regulation No. GR-581, impacting income derived from employment or individual services.

Under GR-58, an effective tax rate or ETR ( tarif effective ratarata, ‘TER’) is directly applied to gross income earned from January to November.

Further, the regulation re-classifies PTKP groups into three categories. We’ve compiled the recent categories and effective tax rates for your reference.

Calculating Monthly Withholding Tax (2024 Regulations)

In general, there are three methods used to calculate PPh 21: the Nett, Gross, and Gross-Up methods. We covered each calculation separately in our guide to Pph 21. The article covers the 2024 process as well as detailed examples for each method.

To summarize the post, let’s determine monthly tax withholding using the nett calculation method:

- Calculate all income earned during the tax year to derive their gross income.

- To determine how much an individual makes in a year, you can refer to the withholding tax receipt (form 1721).

- Apply the progressive tax rates listed above.

As we’ve highlighted the nett income method, the employee’s take-home pay stays as is.

While the government’s goal is to simplify monthly tax calculations, it does not make the process less prone to errors.

Hundreds of employees require monthly tax calculations – not to mention the need to reconcile it by the end of the year – making the process a massive challenge for even the most seasoned professionals.

And remember, tax calculations may vary per employee type. For example, here are some key considerations:

- Married women may opt to perform tax rights and obligations together or separately from their husbands.

- Resident taxpayers without an identification number (NPWP) are subject to a surcharge of 20% on top of normal tax rates.

- Expat workers (non-residents), on the other hand, are subject to a general withholding tax (WHT) of 20% of their Indonesian-sourced income (Article 26 of the Income Tax Law).

We highly recommend that you automate payroll processes or outsource the work for better accuracy.

Filing Monthly Taxes

You’re required to pay monthly income taxes on the 10th of every succeeding month. Moreover, the tax return filing deadline falls every 20th of the following month.

Employers must give employees the WHT Tax Slip. The slip is used to file their Annual Individual Tax returns. Individuals can use Article 21 WHT as a credit towards their tax payment.

2. Year-End Tax Reconciliation

While taxes calculated from January to November are subject to ETR/TER, continue to apply the standard process for annual calculations in December.

To recap:

- You’ll need to determine the employee’s annual gross income.

- Apply deductibles such as operating expenses, jaminan hari tua (JHT), jaminan pensiun (JP) to get the net income.

- Deduct PTKP from net income and apply the corresponding tax rates to get the annual PPh 21.

- Deduct the annual Pph 21 by the total income tax from January to November. The number derived is your employee’s December tax payable.

Now, it’s important to note that this regulation could end up with tax over- or underpayments by December. So ensure that you’ve communicated all possible scenarios to employees ahead of time.

3. Submit Annual SPT Forms

Based on their income, individual taxpayers are required to complete one of three Annual SPT forms:

1770-SS Form (For private employees)

– Applies to taxpayers earning a gross annual income not exceeding 60 million IDR.

– Permanent employees need to complete specific fields, including personal information and income tax details, and attach proof of withholding tax, as this form transfers data from Form 1712 A1 (private workers) and Form 1712 A2 (civilian workers).1770 Form

– Applies to residents who earn income from a business, investment, overseas income, or capital gains.

– Even individuals with no income can use the form by indicating “0” in the income column with a statement letter.1770-S Form

– Individual taxpayers who have a gross annual income of 60 million IDR or more.

-Income is derived from domestic ventures such as interest, royalties, rent, or properties. Intended for workers with income from at least two workplaces.

Payment Deadline – No later than the end of the third month after the year ends before the tax return is filed.

Filing Deadline – End of the third month after the tax year ends.

4. File Withholding Tax Forms for Employees

There are two types of withholding tax forms for employees:

A. 1721-A1 for private employees

B. 1721-A2 for civil servants

Form 1721-A1 only applies to permanent employees reporting their income tax returns.

It serves as proof of deductions throughout the fiscal year or for as long as the employee continues to work for the company during the fiscal year.

Form 1721-A1 must be completed by the employer, and then given to the employee no later than January of the following year.

Penalties for Late Filing and Payments

Late Filing

Note that individual or corporate taxpayers may request to extend the filing of the income tax return for a maximum of two months after the statutory deadline.

Failure to file a tax return by the deadline may result in a warning from the DGT. Warnings typically require the taxpayer to file the tax return within 30 days of the warning letter date.

If the corporation or taxpayer fails to adhere to these deadlines, a penalty of 100,000 IDR shall be imposed.

Late Payments

If taxes are not paid on time, you’ll have to pay a penalty. Penalties are subject to interest rates, calculated based on the amount of tax you failed to settle and the interest rates set by the Ministry of Finance (MoF).

Make Your Year-End Payroll Compliance List – And Check It Twice!

As your workforce expands, businesses face a growing number of tax requirements and calculations alongside their existing workload.

Not to mention, companies handling unique work conditions like contract work, retroactive pay, and foreign employees must adapt their calculations accordingly.

The good news is, you don’t have to stick to spreadsheets or outdated systems. Ensure year-round compliance with KAMI’s payroll solution. We’re rolling out the latest PPh 21 regulations to our system so you can easily calculate monthly tax payables.

KAMI also ensures accurate tax calculations for varying work conditions and easy access to annual tax filings (Form 1721-A1), allowing HR and finance teams to focus on strategic tasks.

Talk to an expert today to learn more about our DIY and do-it-for-you payroll solutions.