Income tax is imposed on individuals or entities on income received within a tax period.

An income tax that HR teams need to get ahead of is stipulated on Article 21 (“PPh 21”) of the Income Tax Law and 2021’s Harmonization of Tax Regulations Law.

More recently, the Indonesian government issued regulation No. GR-581, impacting income derived from employment or individual services.

In this article, we’ll explore the general changes to calculating employee withholding tax.

Indonesia’s Income Tax Law: PPh 21

In principle, PPh 21 is a withholding tax imposed on income received by a domestic Individual Taxpayer (Wajib Pajak Orang Pribadi/WP OP) for the work, services, or activities he/she performs.

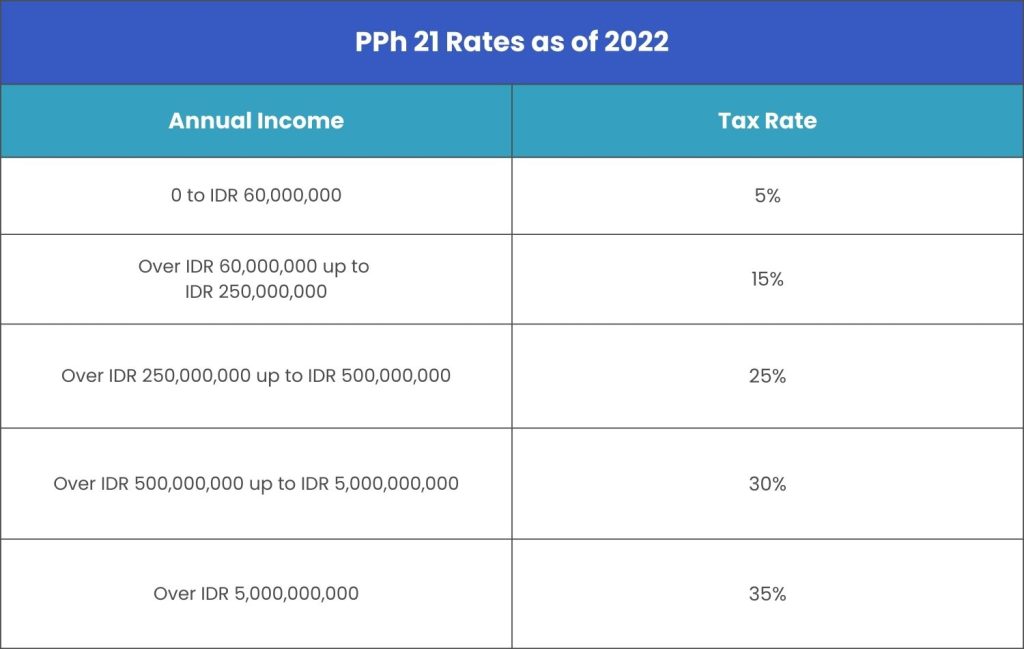

PPh 21 has a progressive rate based on the income obtained by taxpayers.

These are the previous tax rates until the changes announced last December 27:

We’ve compiled the latest categories and the applicable monthly effective tax rates (ETR) for each income range.

What else has changed under Pph 21 regulations?

1. Monthly withholding tax calculation – An ETR/TER shall be applied for calculations ranging from January to November.

2. The ETR/TER under GR-58 is directly applied to the individual’s gross income for a specific month.

3. Reconcile taxes by the end of the year – The annual tax calculation done in December still follows the stipulated progressive income tax rates under Article 21.

To calculate the final tax underpayment, subtract the December recalculation from the total tax withheld from January to November.

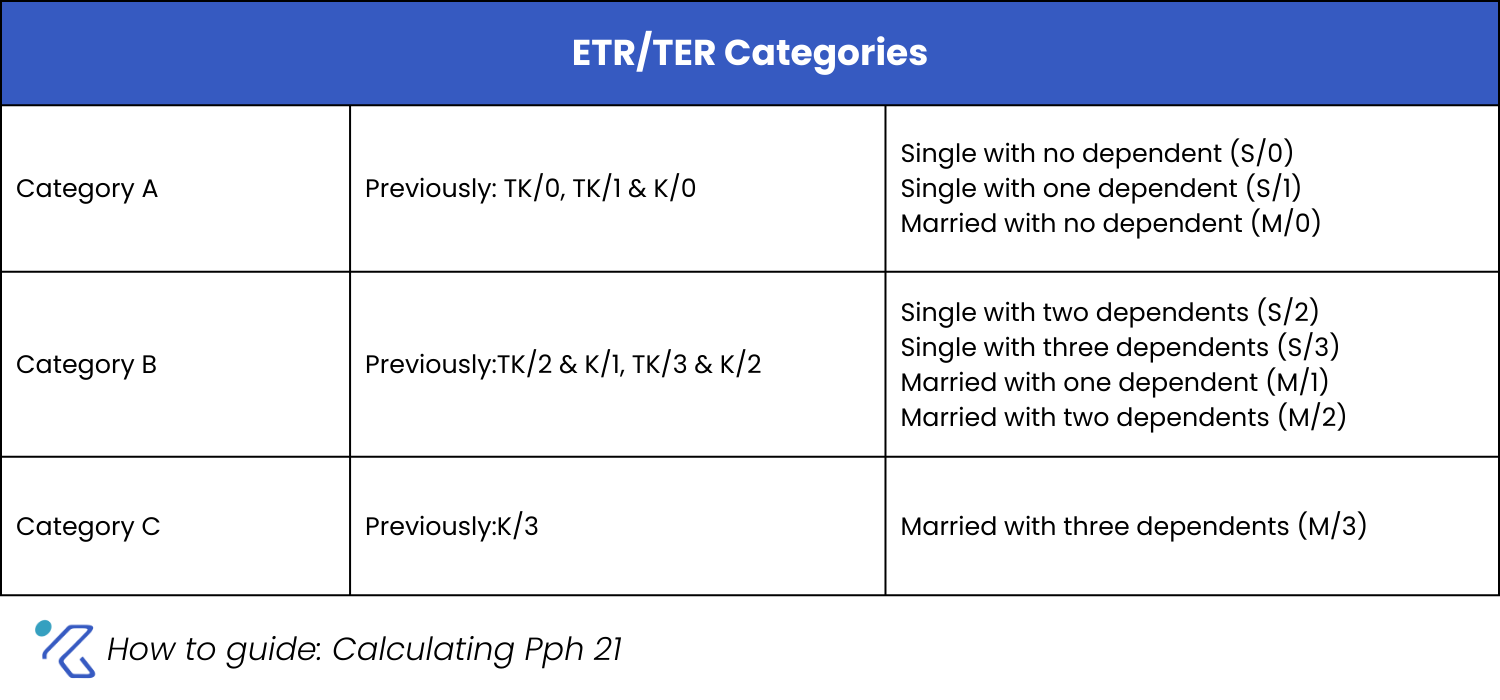

4. Changes to PTKP groups:

5. A daily ETR is applied to income received by non-permanent employees on a daily, weekly, or unit-rate basis. Apply the following ETR on daily income rates:

5. A daily ETR is applied to income received by non-permanent employees on a daily, weekly, or unit-rate basis. Apply the following ETR on daily income rates:

- 0% for daily income up to IDR 450,000

- 0.5% for daily income above IDR 450,000 up to IDR 2,500,000

As of writing, the government does not regulate an ETR for daily income above IDR 2,500,000.

Non-taxable Income (PTKP)

Non-taxable income is a threshold that determines whether a person is obligated to pay income tax or not. In addition, non-taxable income also serves as a deduction in calculating tax payable.

Based on the Harmonization of Tax Regulations Law, the non-taxable income is as follows:

- 54,000,000/year Rp. for individual taxpayers;

- 4,500,000/year Rp. or 375,000 Rp./month additional for taxpayers who are married or have a family;

- 54,000,000/year Rp. or 375,000 Rp./month for individual taxpayers who are married with a joint income; and

- 4,500,000/year Rp. additional or an additional 375,000 Rp. per month for each blood family member and family by marriage in a straight line and adopted children who are fully dependent, a maximum of 3 people for each family.

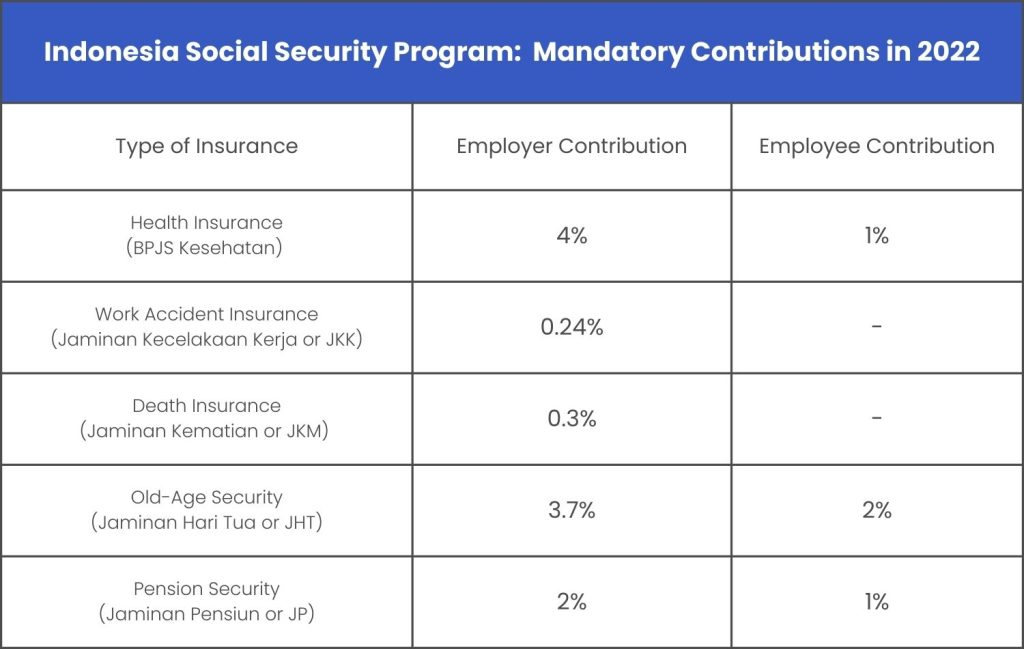

Healthcare and Employee Social Security Contribution

A company that participates in the Healthcare Social Security and Employee Social Security programs must pay the following contributions (minimum rates):

Note: As of 2021, the maximum amount of JP is IDR 87,546.

Functional Cost Deduction

Functional cost refers to collected, earned, and maintained income from specific business activities.

Indonesian laws and regulations stipulate that the company can impose occupational expenses a maximum of 5% of the gross income per year or a maximum amount of IDR 500,000 per month.

After you consider the above aspects, the next step you should take is to determine what calculation method you want to implement.

Applying the Latest PPh 21 Calculations: Nett, Gross, and Gross-up Methods

The difference in the PPh 21 calculation method impacts the employee payroll and company expenses. To get a better grasp of PPh 21 calculation and the differences between each method, check out the examples below.

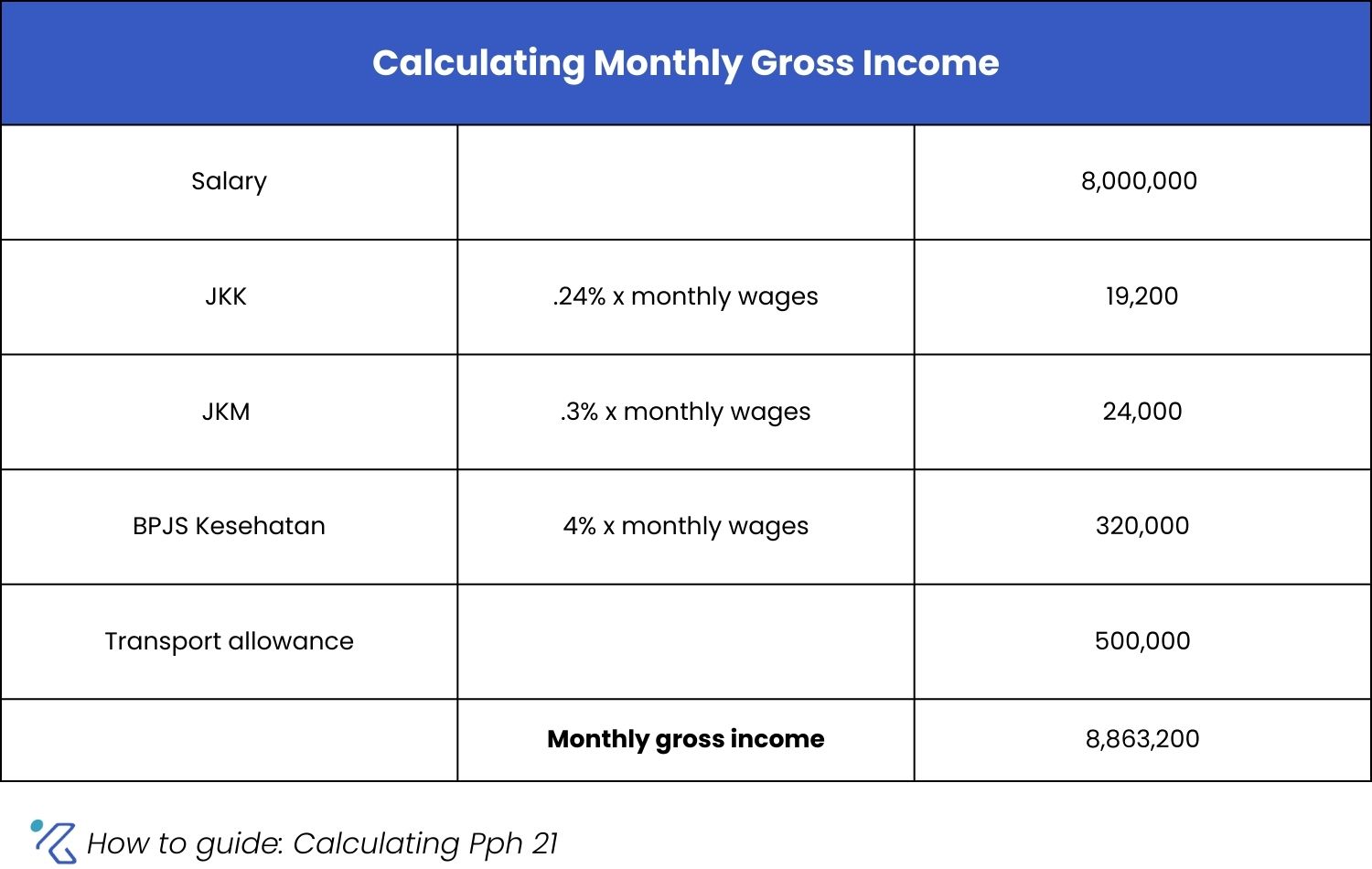

We will calculate an employee tax with an offered income of 8,000,000 Rp. This employee will fall under Category A or no dependents. They are to receive a transport allowance from their company.

Note that we simplified the calculations below. Your monthly calculation may vary depending on the employee’s income earned (commissions, bonuses, etc.).

Nett Calculation Method

Nett calculation is a tax withholding method where the company bears the taxes of its employees.

1. Determine the employee’s monthly gross income.

2. Calculate the income tax based on their category and corresponding ETR.

A. This employee’s range will fall under category/TER A (1.75%).

B. Multiply the gross income by the ETR.

Calculation: 8,863,200 Rp. x 1.75%

Monthly PPh21 = 155,106 Rp.

3. Since the company covers the employee’s taxes in this method, the take-home pay will stay as is (8,863,200 Rp.).

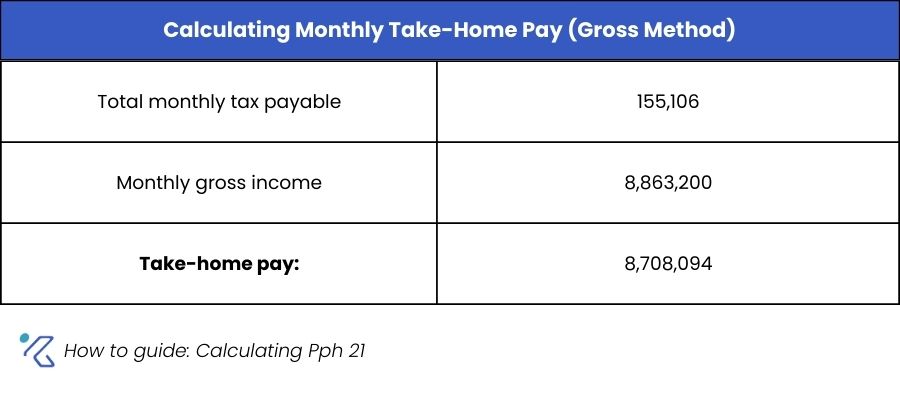

Gross Calculation Method

In the gross calculation method, employees bear their income tax amount.

1. As we did above, calculate gross income.

2. Again, let’s calculate the income tax based on their tier and corresponding ETR.

Ter A Rates: (1.75%)

Calculation: 8,863,200 Rp. x 1.75%

Monthly PPh21 = 155,106 Rp.

3. As this is the gross calculation method, taxes shall be borne by the employee.

So to calculate take-home pay, deduct their total monthly income from their monthly income tax.

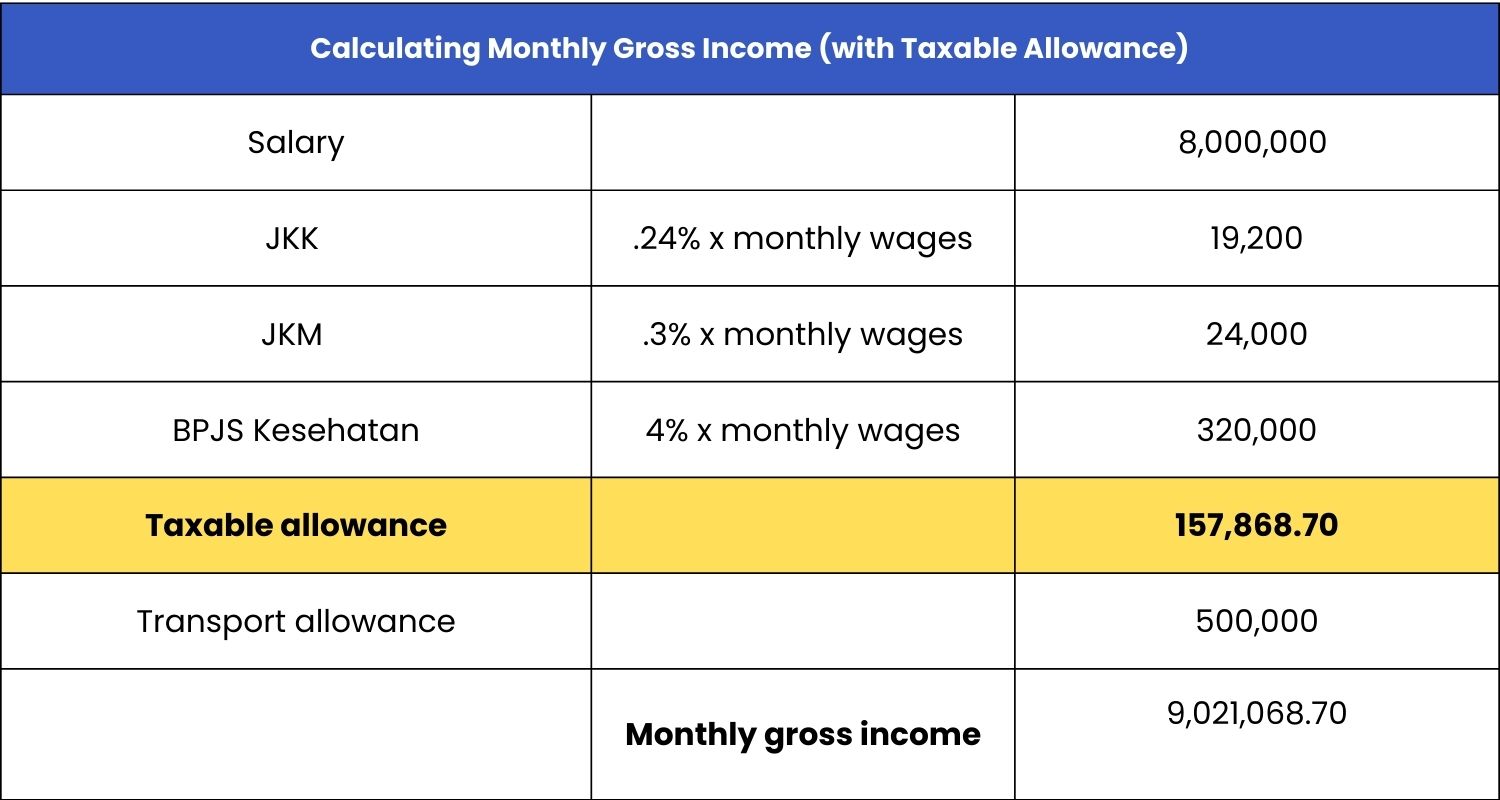

Gross-up Calculation Method

The gross-up calculation method is where the company provides tax allowance to the employee.

Once again, we’ll use our initial example for this method.

- Calculate monthly gross income together with their taxable allowance.

2. Proceed to calculate PPh21 by multiplying the corresponding TER by the gross income above.

Calculation: 9,021,068.70 x 1.75% = 157,868.70.

3. Calculate the take-home pay by deducting the monthly income tax from their gross income.

Calculation: 9,021,068.70 – 157,868.70= 8,863,200Rp.

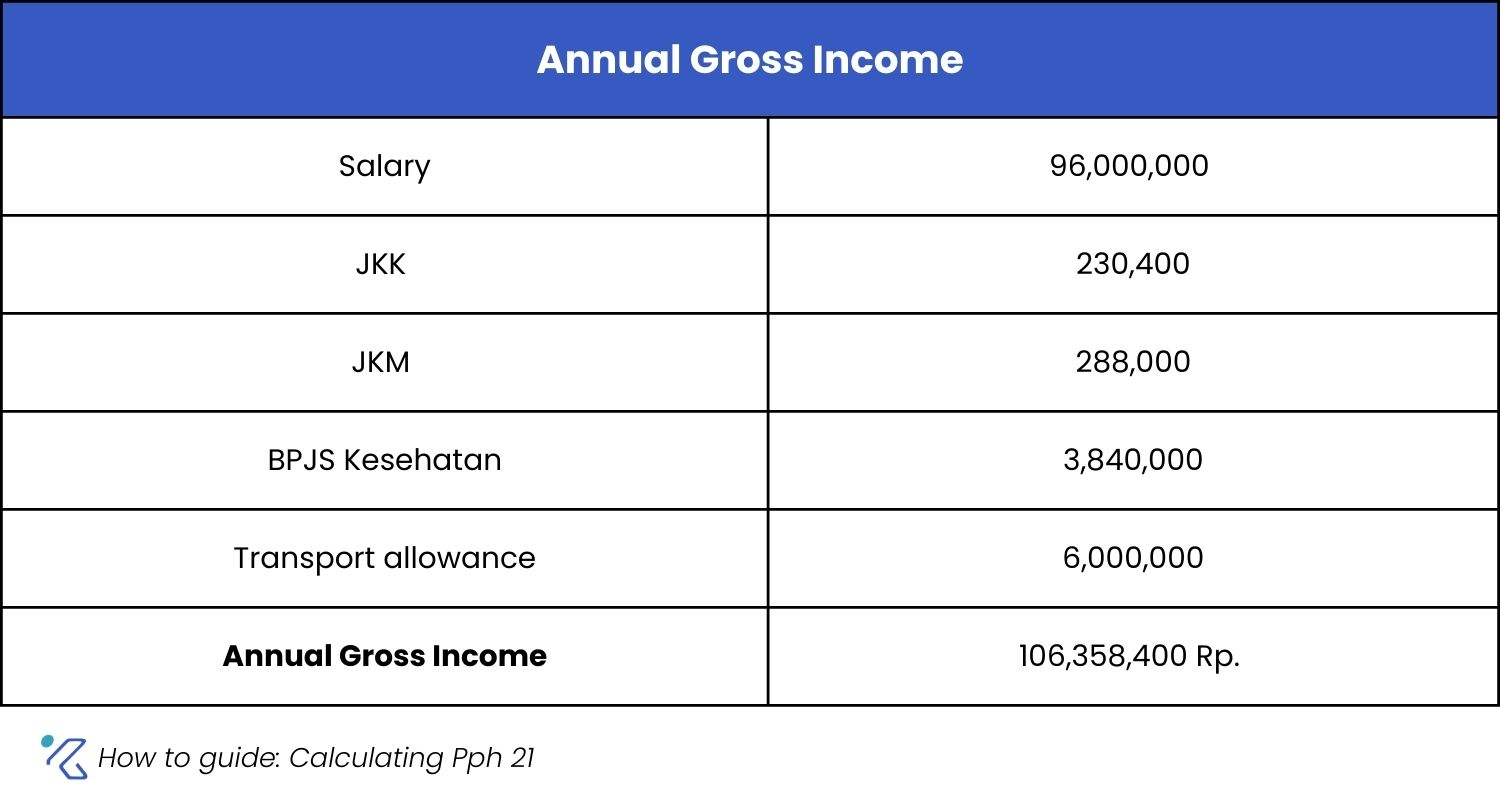

End-Year Income Tax Calculation

In the updated regulations, there are no PTKP deductions applied monthly. These deductions shall be reconciled by the end of the year.

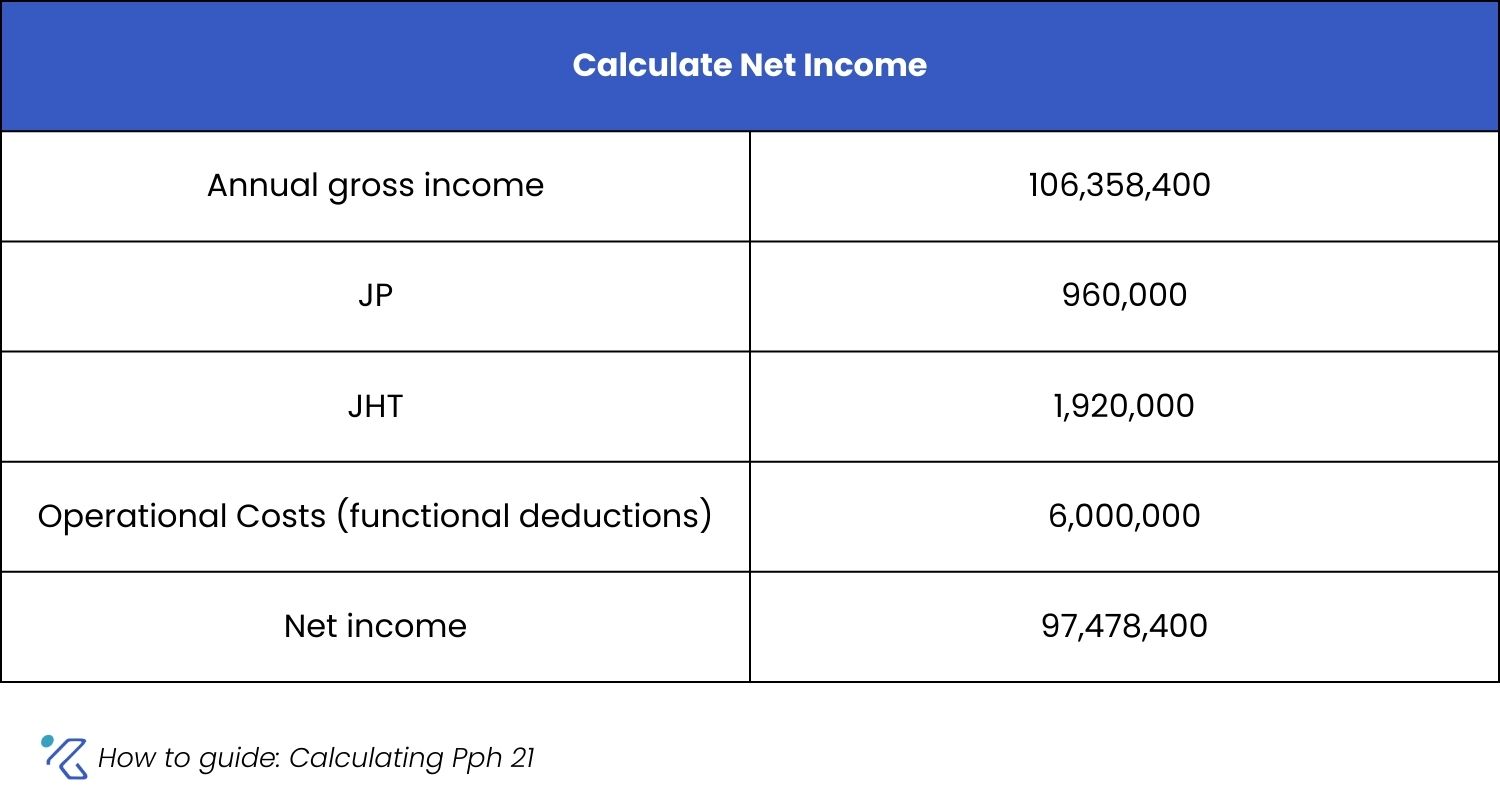

- Determine the annual gross income.

2. Apply functional, JHT, and JP deductions to determine net income.

3. Deduct PTKP from net income and apply tax rates to get the annual PPh 21.

A. Deduct your PTKP from the net income

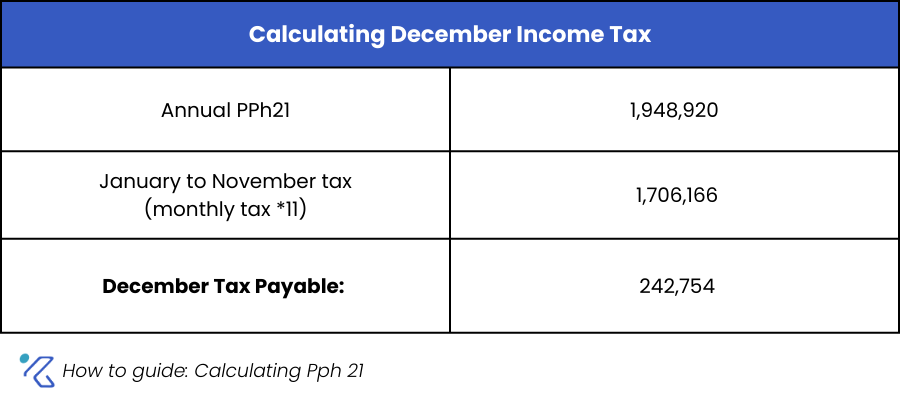

97,478,400 – 58,500,000 = 38,978,400 Rp.

B. Multiply it by the employee’s tax rates.

Annual tax: 38,978,400 x 5% = 1,948,920 Rp.

4. Determine the income tax from January to November and deduct it by the annual Pph21 to obtain the employee’s December tax.

Comply with Changing Regulations

Are these calculations too complicated? Don’t worry!

Our KAMI system is now updated with the latest Pph 21 categories and the applicable monthly tax rates so you can easily calculate employee taxes automatically with the method of your choice.

You could also manage complex allowances, commissions, bonuses, and deductions with ease. KAMI also understands that ever-changing regulations impact your payroll, but our hyperflexible system is built to help you comply anytime.

On top of that, it’s built with large businesses and enterprises in mind, so can process thousands of payslips in minutes.

Talk to an expert today to learn more.